Silver, What is The truth, the whole truth, and nothing but the truth?

Is the Silver Market Trading on Fundamentals — or Flow?

What happens when a large quantitative firm or High Frequency trading firm enters the silver market? Traditional bank activities of managing internal order flow and trading in concert to client positions as the middle man begins to change to market activities where risk takers are rewarded directly. The middleman becomes obsolete and quant firms begin automated or algorithmic programs to trade directly against retail or institutional order flow. Strategies are no longer traditional secular bets but rather complex relative strategies where losing money on one side is the cost for making money on the other side of the trade. Taking a position in the underlying investment such as Silver iShare Trust (SLV) opens Pandora’s box to multiple other mind blowing strategies using options and derivatives.

The Evolution of Silver Trading: From Hedging to High-Frequency Strategy

In this case, using the underlying SLV ETF, sophisticated traders at large trading firms with large pools of capital to effectively entertain option strategies that capitalize on the embedded leverage puts and calls provide. In other words, using the underlying asset to impact order flow while establishing option positions, which on a magnified scale, provides untold degrees of leverage and earning capabilities.

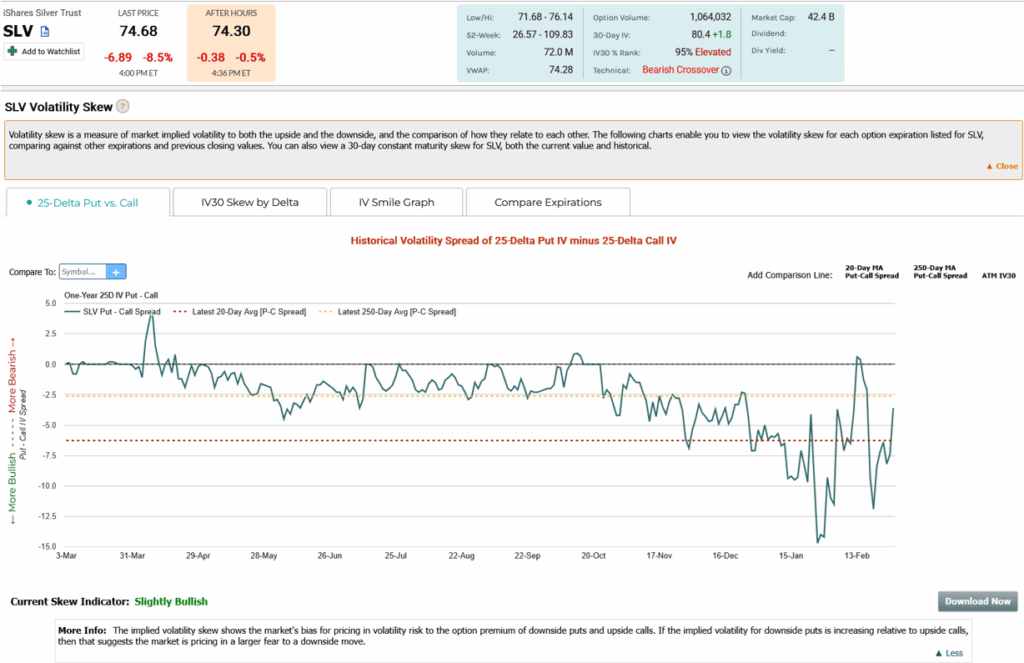

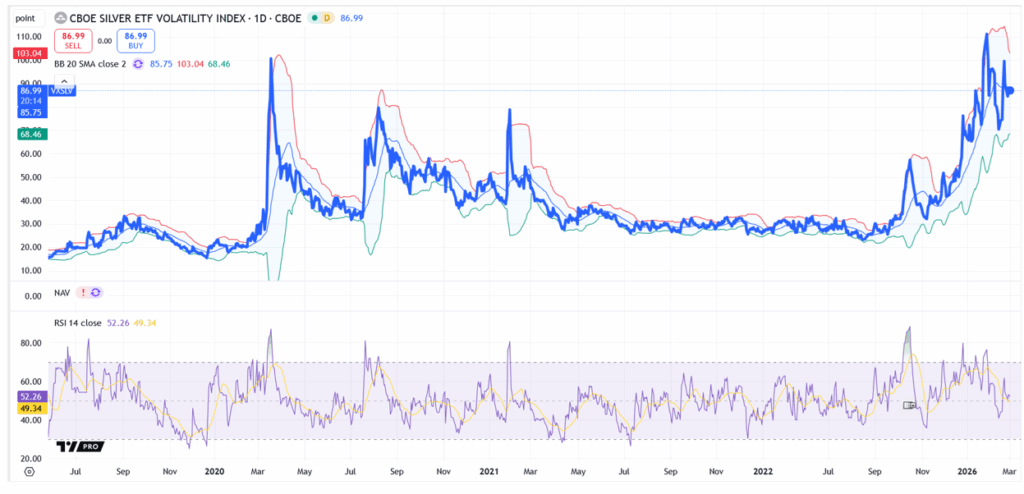

Complex option activities can be instituted to take advantage of rising implied volatility of an underlying asset or option. In turn, that rising implied volatility makes option premiums more expensive and more profitable to the sophisticated trader. Unlike the retail public that attempts to use options for spreads or secular direction, sophisticated trading firms will use the positioning, borrowing, and trading of the underlying asset to actually drive earnings from leverage derivatives at multiples than what the underlying could provide. Below we see massive fluctuation in volatility skew for SLV ETF. The volatility of big changes in bullish to bearish bets may be the product of using the underlying SLV ETF to push the market in one (ultra short term) direction while that sophisticated trading firm built an option position for a directional move in the opposite (slightly longer term) direction .

“Short Against the Box”

Lets use an example of an old Wall Street Strategy that has been restricted from a tax perspective (Taxpayer Relief Act of 1997).

A short sale against the box involves selling short stocks you already own to create a zero net position. A short sell against the box involves shorting a stock you already own without selling your existing long position, creating a neutral offset where gains and losses cancel out. This approach was once used to defer capital gains taxes, but the Taxpayer Relief Act of 1997 and later SEC/FINRA rules made using it for tax avoidance illegal. Shorting against the box is a way to avoid realizing capital gains, but it requires separate accounts for long and short positions.

The SEC and FINRA have imposed regulations, including the alternative uptick rule, limiting when shorting can occur.

However, when a HFT or algorithmic trading firm takes an enormous underlying long position in a stock, the strategies and profits from using options can multiply the earnings capabilities. Buying options and betting on the secular action is one method of making money. Using spreads and other sophisticated strategies are another way. However, when a large trading firm can use the underlying asset to drive momentum and implied volatility a whole new world of profits opens up. Volatility premiums begin to rise and fall at accelerated levels. Gaming these sensitive and rapid changes in value using the volume and leverage of options turns a few dollar move in the underlying into an infectious move of increasing volatility that attracts the madness of crowds.

In addition, a gamma squeeze is a rapid, often extreme, surge in a stock’s price caused by intense call option buying. As retail investors buy large volumes of out-of-the-money calls, market makers who sold them must hedge by buying the underlying stock, creating a positive feedback loop that drives prices higher, often resulting in significant, rapid gains followed by sharp declines when the frenzy subsides.

These types of mania can be the product of a large trading firm using their enormous underlying long position as a bank to borrow against these shares and effect short sales that then allow a firm to build an option position counter to the artificial decline in the underlying’s sell off from short sale activity. In essence, any loss of short sales is the cost of doing business for making multiples of money by trading the options for a more powerful move in the opposite direction. Taking advantage of increasing option volatility premiums allow an advantage over trading the simple underlying position.

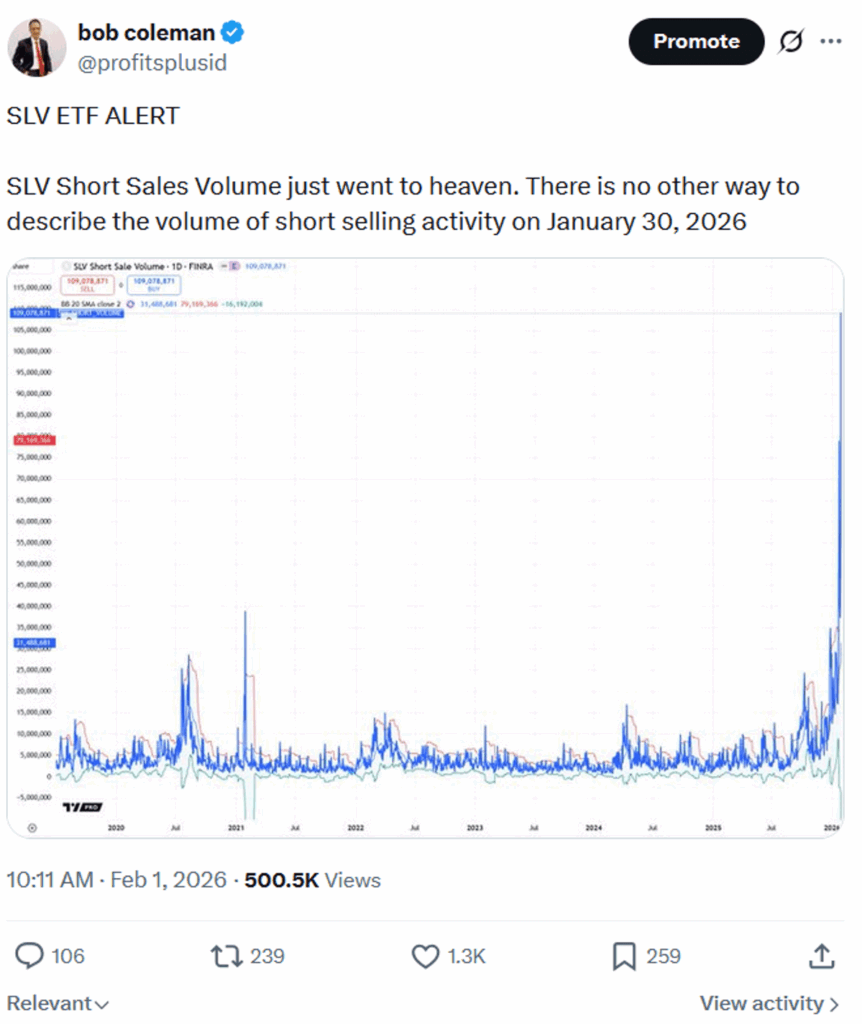

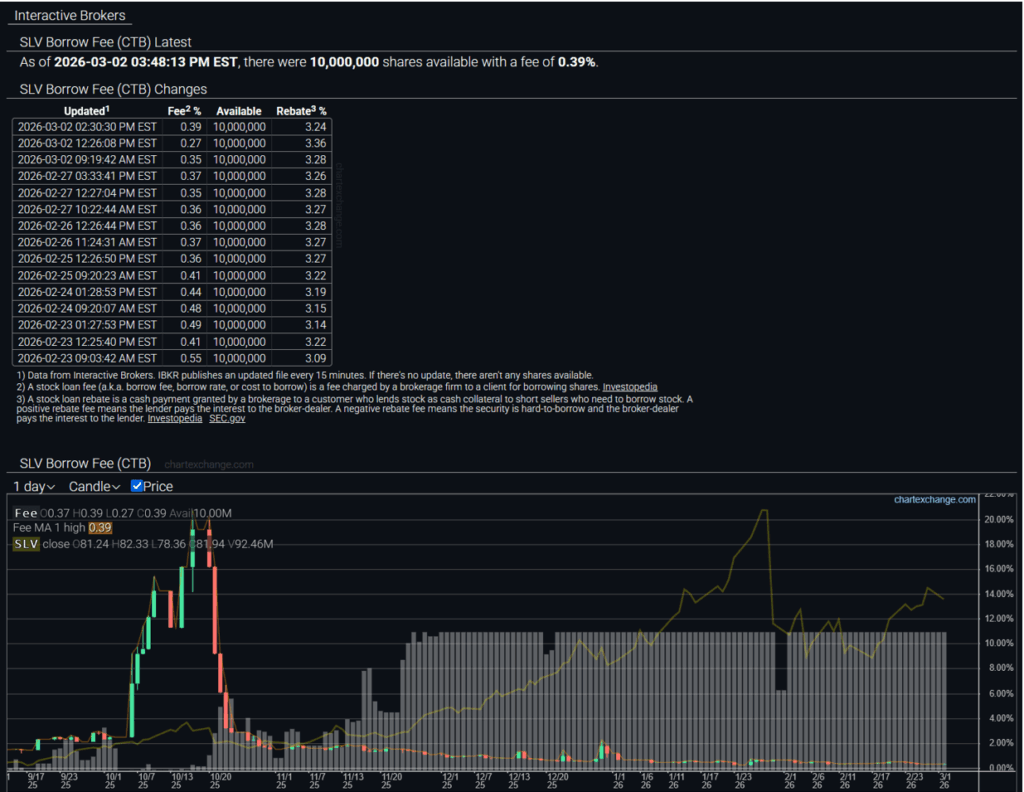

The following saw enormous volumes of short sale activity toward the end of 2025 into 2026.

Short Interest Anomalies in 2025–2026

Short interest in the SLV ETF rose steadily through 2025, even as the price for the underlying shares rose as well.

Short Interest Anomalies in 2025–2026

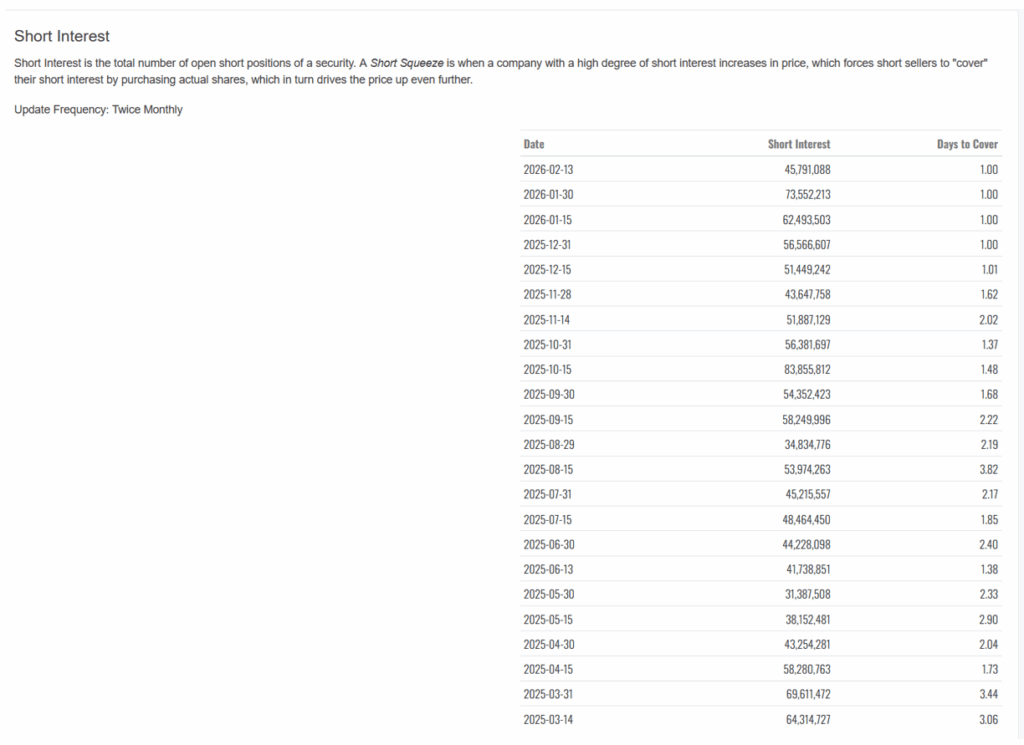

We saw the effects of a major squeeze in silver in October 2025. Borrowing rates to short shares blew out to as high as 20% when normally they were .4%.

However, something odd happened in December 2025 into January 2026. While SLV continued to race higher, short sale activity rose at the same time. The squeeze higher in SLV’s price did not show the traditional effects of high borrowing rates and lack of shares available to borrow as short sales volume exploded. In fact, SLV shares available to borrow were at multiple levels (10 million shares) in January 2026 versus October 2025 (100,000 shares). During the same respective time frames, the borrowing fee to short shares had collapsed.

Implied volatility also rose at an accelerated rate in December 2025 and January 2026. In fact implied volatility doubled from the October highs. What would cause such an event where the underlying was going higher with increasing short sales volume and borrowing fees to short shares were crashing lower?

If a trading firm took a sizable, long position and used those shares as a way to borrow shares too short, the borrowing fee may not change and the pool of shares available to borrow would increase. Using both the long and short positions in the underlying could then be used to affect a strategy using options to profit from increasing volatility. Essentially, one strategy could be to short shares in the morning, driving down the share price, while building call positions which were being bought up not only as intrinsic value was declining but also declining implied volatility values. We saw a pattern of sharp declines in SLV ETF price in the morning, only to reverse later in the day or the next day. We also saw a pattern of rising implied volatility with rising prices in SLV ETF. The reason is very compelling to use SLV ETF shares as a catalyst to effect outsized returns in the options markets.

ETF Market Structure: Creation, Redemption, and Authorized Participants

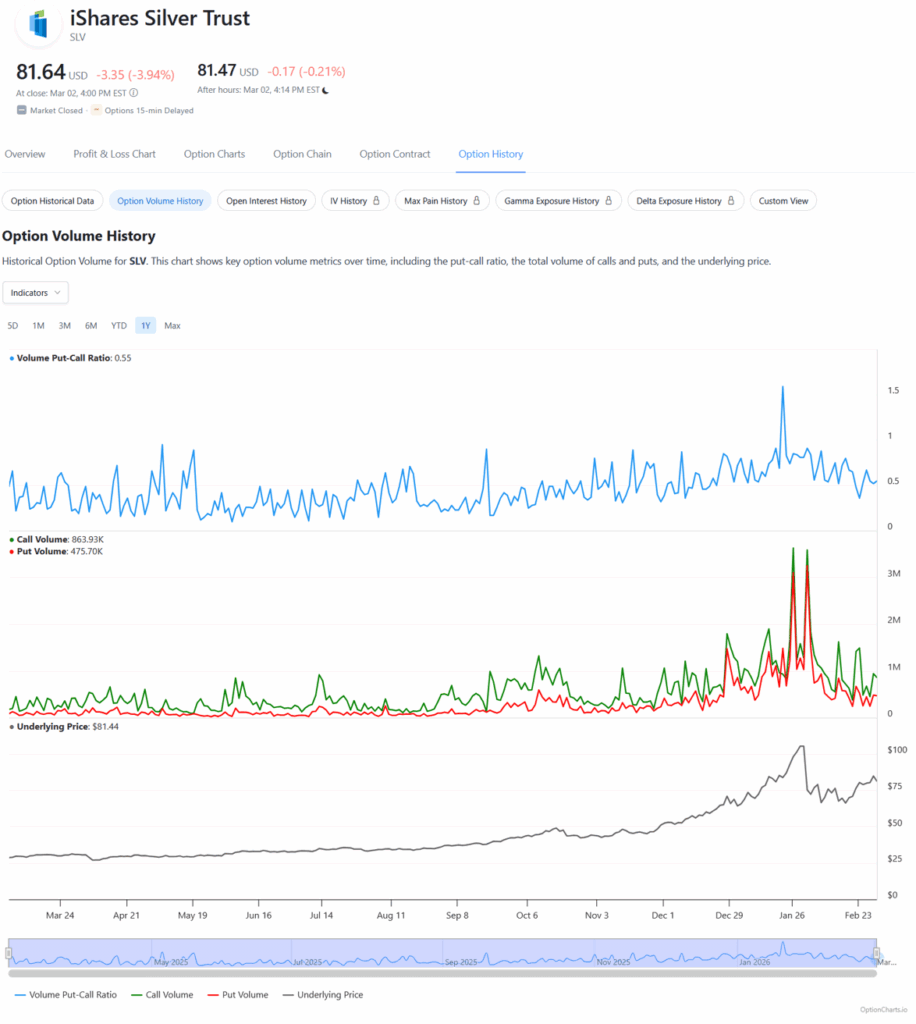

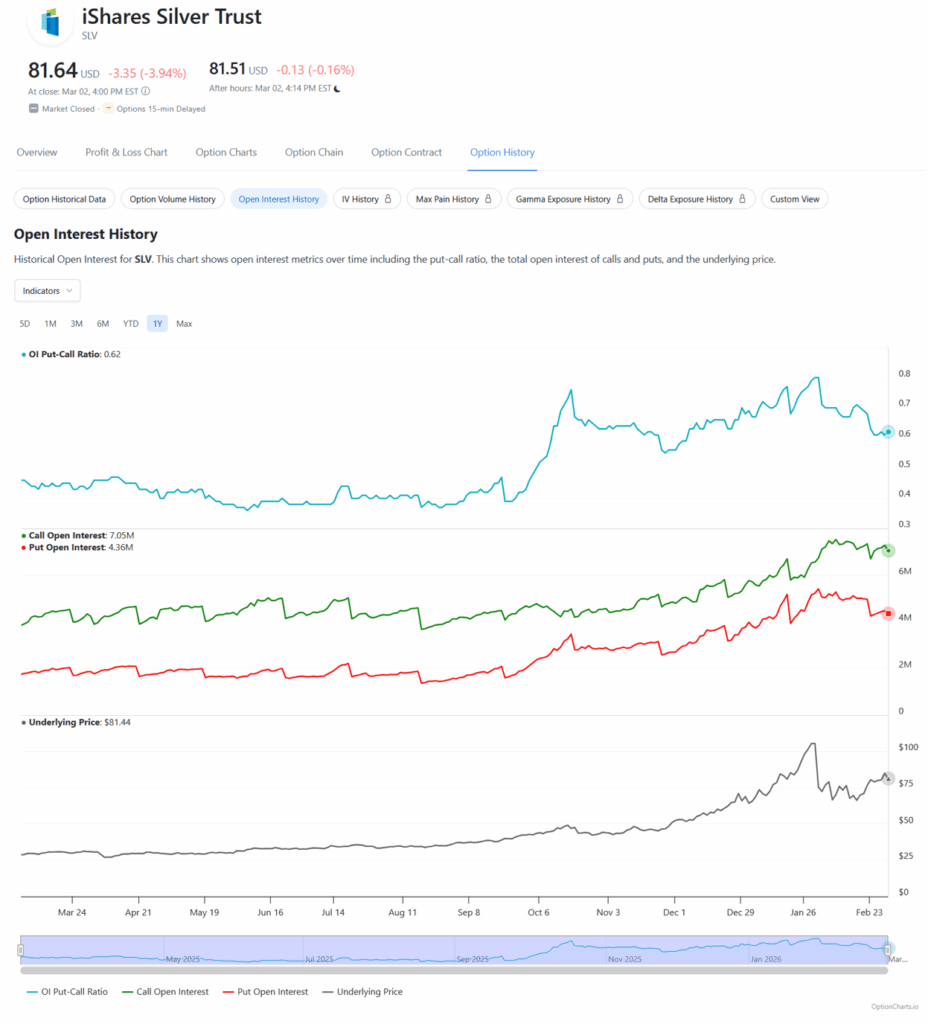

Lastly, the following charts show put and call trading volume and open interest. These charts may support the idea that such a potential strategy employed by an HFT or algorithmic trading firm becoming one of the largest shareholders in an ETF to influence and attract greater attention and trading activity from broader participants. Greater participation increases liquidity and depth in both the underlying equity and options markets. Larger trading volumes allow for larger lucrative position sizes. If the order flow can be amplified to make the trade even more money, why not!

Are Silver Investors Buying Exposure — or Supplying Liquidity?

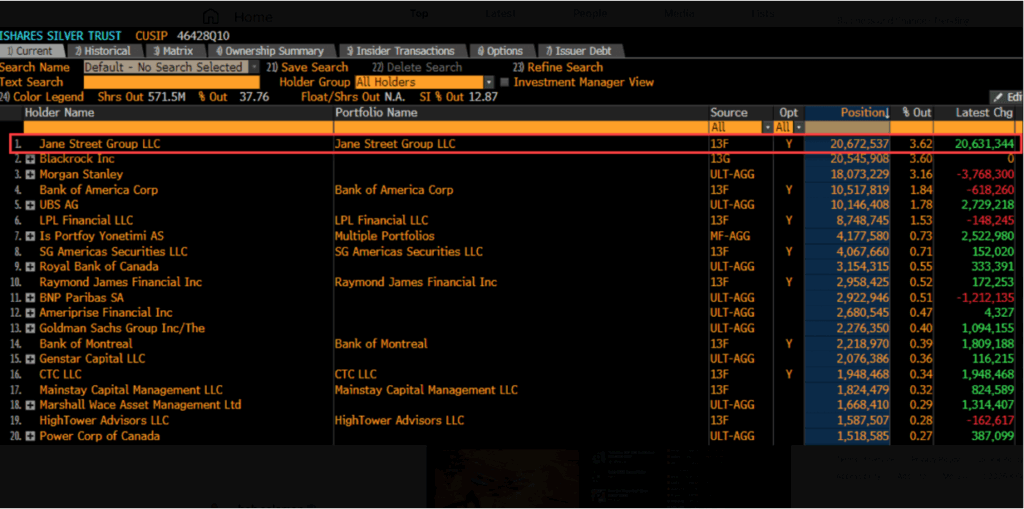

In conclusion, this is an opinion from a market observer trying to make sense of the silver market. Instead of determining whether I am making this up for conspiracy’s sake , let’s look at the facts as reported on https://fintel.io/so/us/slv/jane-street-group-llc

Large Institutional Positioning: The Jane Street Disclosure

Let’s zero in on the following statement.

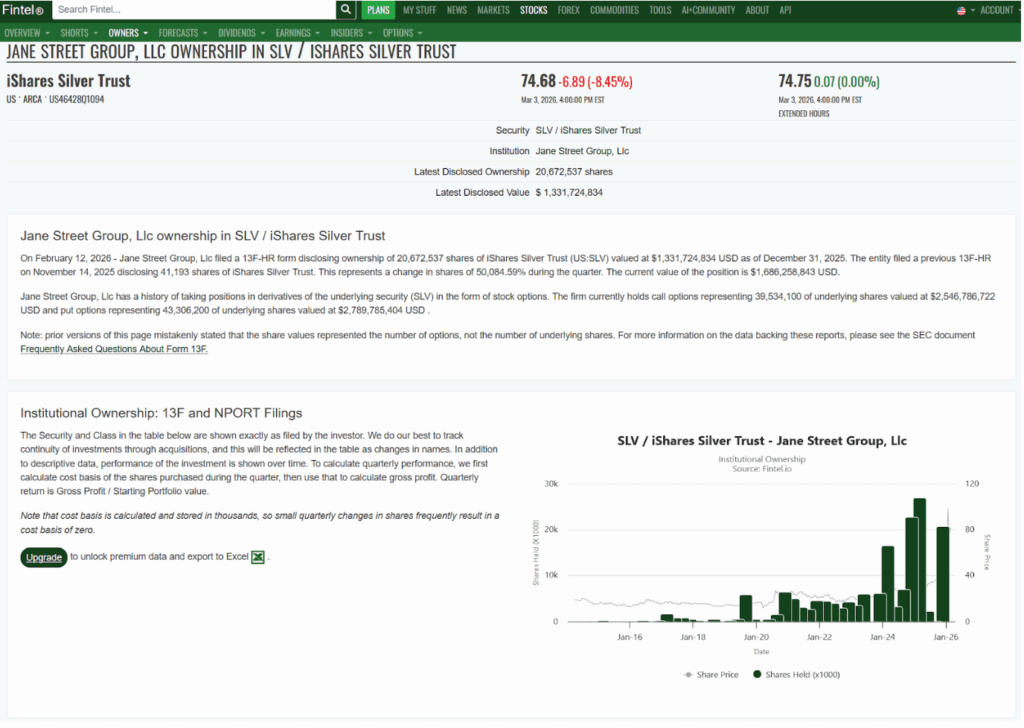

Jane Street Group, LLC ownership in SLV / iShares Silver Trust

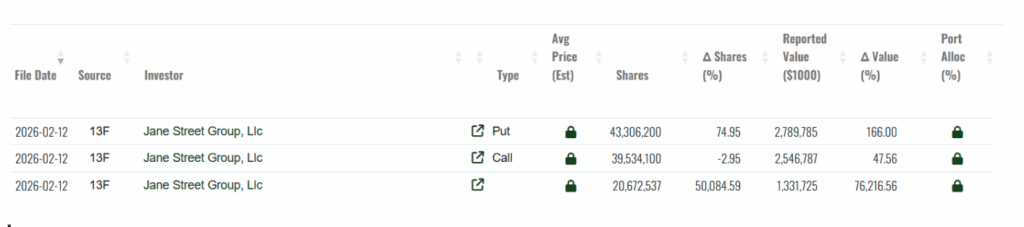

On February 12, 2026 – Jane Street Group, Llc filed a 13F-HR form disclosing ownership of 20,672,537 shares of iShares Silver Trust (US:SLV) valued at $1,331,724,834 USD as of December 31, 2025. The entity filed a previous 13F-HR on November 14, 2025 disclosing 41,193 shares of iShares Silver Trust. This represents a change in shares of 50,084.59% during the quarter. The current value of the position is $1,686,258,843 USD.

Jane Street Group, Llc has a history of taking positions in derivatives of the underlying security (SLV) in the form of stock options. The firm currently holds call options representing 39,534,100 of underlying shares valued at $2,546,786,722 USD and put options representing 43,306,200 of underlying shares valued at $2,789,785,404 USD .

Conclusion: Silver in the Algorithmic Age

To all silver investors wanting simple representation in the price of silver, SLV ETF may provide that. However, in my opinion, investors may not realize when they are buying the silver ETF product, they themselves have become the product. As investors and traders participate and support the order flow in ETFs, Authorized participants profit from the redemption and creation mechanism. What investors and traders may not have been aware of was the possibility of a firm creating and using order flow to benefit from unique short term strategies that obfuscated the trading conditions and fundamentals of the silver market for their gain.

Meet the Author

Bob Coleman, with a successful career in investment and portfolio management since 1992, is the founder of Idaho Armored Vaults and Profits Plus Capital Management, dedicated to providing secure and comprehensive solutions for precious metal investment and storage, emphasizing transparency, risk mitigation, and client-focused service.

BOB COLEMAN

President

(208) 468-3600

[email protected]